Valuation of Cryptocurrencies: A brief analysis of three valuation approaches and their implication on current market developments

Carlos Arad, FinTech Analyst, micobo GmbH & Shourya Nandi, FinTech Analyst, micobo GmbH

June 2018: micobo Research

1. Introduction

The cryptocurrency market has experienced rapid growth since 2017 (Market cap is almost 3x the value of June 17). The question has been raised in how far the market price developments are justified.

This paper will cover the main valuation frameworks developed for application on cryptocurrencies. The models developed and used to quanitfy value of crypto assets are a useful way to think and analyze current state of those assets but should not, by themselves be regarded as a justification for investment as the crypto market is subject to high volatilities, infrastructural changes in the underlying blockchain technology and last but not least, to political and regulation-related risk factors.

Equity investments are made by applying fundamental analysis using finanical statements to analyze publicly traded companies. In the case of cryptocurrencies we can’t use information like that because there simply is none. Therefore we have to change the perspective of valuation into a cost perspective or use relative valuation approaches which will be elaborated in the next chapters. The utility of crypto assets does not come from the generation of cash-flows but rather from community participation (miners secure the network and users execute transactions).

Furthermore cryptocurrencies lack in real-world use cases. Certainly, Bitcoin is already in use for online payments in certain shops and Ethereum is the main technical asset in the case of Initial Coin Offerings (ICO) while Ripple has had a great impact in Japan with banks developing a payment platform using ist technology but nevertheless, the long-term impact are still to be evaluated.

The approach starts with a short introduction into defintion of cryptocurrencies themselves and and quantitative evaluation of the overall market which has an highly dynamic character with the strongest development in 2017 with the emergence of the new cryptoecosystem that started in 2009 with Bitcoin.

In the second half of the paper will provide an overview of the valuation approaches and apply real-time data to the frameworks to estimate potential valuation range of cryptocurrencies.

2. Introduction to Cryptocurrency Market

2.1 What is a Cryptocurrency?

Cryptocurrencies are digital money based on a distributed, safe and decentralized payment system that is created by means of cryptographic methods and transfered on a distributed ledger known as a „blockchain“. The blockchain is used to record information, primarily about the balance of every adress. The approach can be extended to lots of applications.

The first cryptocurrency, Bitcoin (BTC), originated with a whitepaper that was published in 2008 by a pseudonym called „Satoshi Nakamoto“. The main goal was to create a decentralized payment system that allows electronic transactions with the absence of intermediary institutions like banks, etc. Blockchain technology allows us to store and transfer money without the need of a central authority.

Bitcoin Mining

Most people obtain Bitcoins by buying them at a cryptocurrency exchange. Besides that, people can get Bitcoin by mining them.

In the traditional fiat currency system central banks regulate money growth by deciding on just printing it. This process does not apply to non-physical monetary values.

The key of operations of a well-functioning blockchain network is that the network should collectively agree on the ledger’s contents. Proof-of-Work (PoW) is the first consensus mechanism developed for the Bitcoin blockchain.

Bitcoin transactions within a certain timeframe are collected in a block (list of transactions data) which has to be validated. Miners get a Bitcoin fee for providing computation power so that the block can be added to the existing blockchain. Miners play a major role in providing security to the database. Within the scope of the mining process the information in the block is transformed to a sequence of letters and numbers (Hash). Every block contains the hash of the previous block which serves as a security feature. If someone tried to manipulate a transaction by changing the block, the hash would change too. The reference in the following block would then not be true meaning that the hacker would need to mine every other block after the manipulated one which would cost an extreme amount of computational power as an invader needs a multiple of power of the existing miners („51% attack“).

For the security measures miners provide by their services, they are rewarded 12,5 BTC per block.

2.2 Quantitative Analyis of Crypto Asset Market

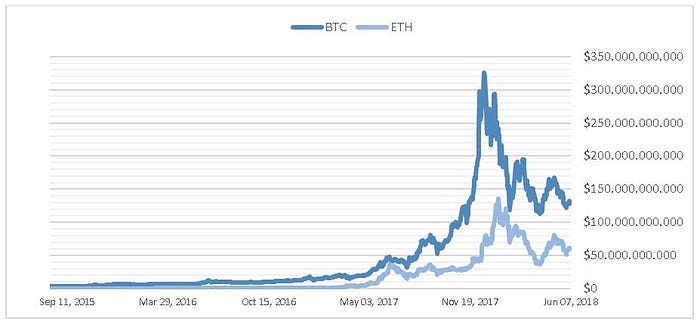

The total cryptocurrency market cap has increased more than 54x since early 2015, reaching approximately $300 bn. in total market cap in June 2018 with 20 cryptocurrencies reaching a market cap higher than $1 billion. Lots of new currencies emerged since the significant public attention and price boost of cryptocurrencies in 2017. New consensus mechanisms (e.g. proof-of-stake) and smart contract systems (e.g. Ethereum blockchain) realize innovative non-monetary use cases (e.g. ICOs).

Market shares‘ historical distribution did undergo significant changes as more and more cryptocurrencies were developed. The largest fraction, Bitcoin lost to Ether (ETH), the native currency of the underlying Ethereum blockchain. Nevertheless Bitcoin still remains the dominant cryptocurrency in terms of market capitalization.

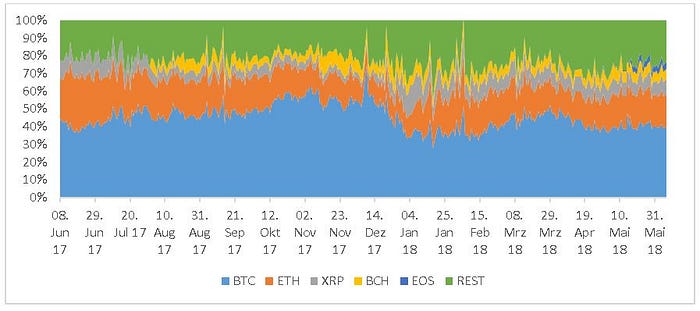

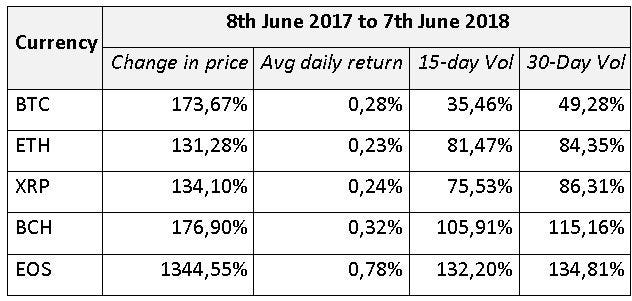

The largest five cryptocurencies Bitcoin, Ethereum, Ripple, Bitcoin Cash and EOS make up for 76,66 % of total market cap as of June 2018 (77,41 % in June 2017). The absolute share did not change significantly in comparison to 2017 but the shares among the currencies did undergo a highly volatile year.

In terms of return, EOS investors gained almost 8x the return Bitcoin investors achieved since 2017. Notably volatility of Bitcoin is the lowest in our study group with EOS showing the highest value for the last year.

3. Valuation of Crypto Assets

Intrinsic value is hard to measure in the case of a cryptocurrencies. Therefore we need to modify valuation methods used for traditional assets like stocks (cashflow/ earnings generating assets). However we can develop several models based on the character of cryptocurrencies and use a consensus average value as valaution outcome, the fair value. High volatility makes it hard to use models like the moving average method as this one suffers from various pitfalls in estimating future prices in volatile environments.

3.1 Net Cost Model

Model Application

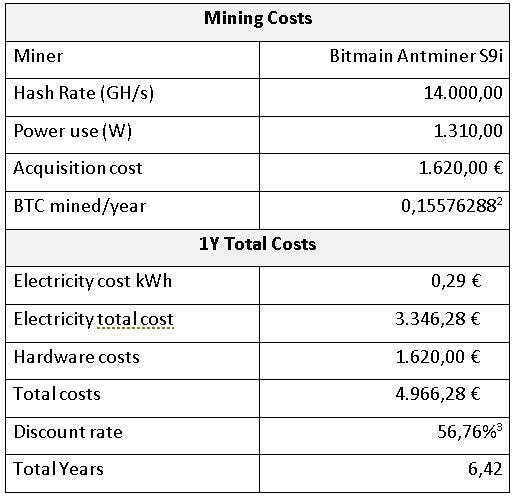

The Net Cost Model (NCM) of cryptocurrency valuation is based on the assumption that a person can either decide to 1) mine bitcoin in order to receive a certain amount of units as a reward or 2) buy them on a cryptocurrency exchange. The goal is to determine a value of indifference between the mining process and a purchase at a exchange. For further computations we will need to determine the components of a exemplary mining process to calculate the amount of cash-outflow in the entire period.

Mining Costs include costs for the hardware and costs for electricity to run the hardware. In this model we use the Bitmain Antminder S9i (1.310W; 14.000 GH/s) as exemplary hardware and rate electrictiy cost at €0,29 kWh (Germany average)[1]. At a current mining difficulty of ≈ 0,155 BTC/Year it should take around 6,42 years to acquire one Bitcoin. Mining difficulty is systematically growing (90 Day Difficulty Change = 50,15 %[2]) meaning that mining cost will raise in the next years.

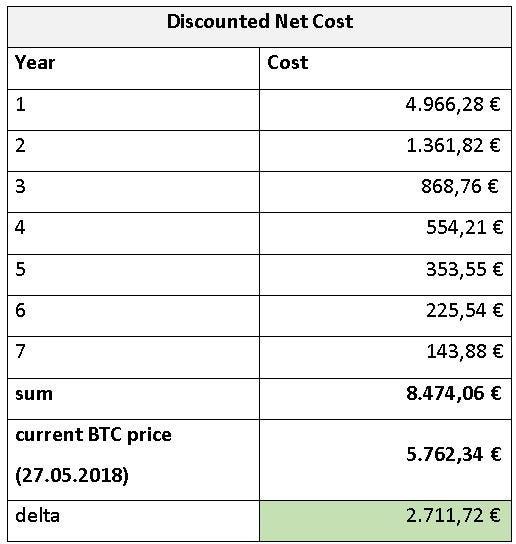

Total cost for the first year sum up to €4.966,28. We assume that the mining hardware will not be sold after the time period in use and that depreciation has no effect on the performance of our hardware. Following this rules the costs after the first year are only correlated with electricity consumption and price changes in the energy market (Hedging instruments to stabalize energy prices will not be considered in this paper).

One block is mined per 10 minutes irrespective of the number of miners. The cryptographic puzzle gets harder if the number of miners increases and decreases if the number decreases. Hence the BTC mined per year fluctuates based on the number of miners. We have considered that the amount of miners remains the same for purpose of this calculation.

Net cash outflow after the first year need to be discounted with an appropriate rate. Therefore we used a basic regression model using the DAX and BTC closing prices to determine the beta value of Bitcoin. From the regression model (Beta of ≈ 4,34) in combination with the current 10Y bond rate (0,445%)and the 4Y average DAX return we derived a total CAPM cost of capital of 56,76 %.

Discounting the numbers with our discount rate we obtain a present value of €8.474,06 of the future cash outflow from the perspective of a miner in the Bitcoin network. The value of a Bitcoin should therefore raise by €2.711,72 (+47,6 %) in order to match the cost structure of a miner. From todays perspective it would be more profitable to just purchase Bitcoin at an exchange like Coinbase instead of relative expensively mining them.

Mining rewards (currently 12,5 BTC per block) will be halfed by 26.05.2020[3]. This implies that reward output for a single miner should decrease by 50 %. This would have an impact on our calculation result as we need to double years until one BTC is mined. At least 6 more years of electricity costs need to be added to the valuation result which leads to a new value of 8.710,48 €. The effect is minor due to the large discount effect.

3.2 Network Value to Transaction Model

Discounted Cashflow methods can’t be applied in the case of Bitcoin. Other absolute valuation principles have to be adopted to the nature of cryptocurrencies.

A relative valuation measure is therefore a good alternative to at least find cryptocurrencies with relatively low price level. An overvalued currency in a overvalued system can ‚at the moment‘ be an undervalued asset. The question is which metric will we use to substitue earnings in the P/E Ratio.

Transaction activity represents the demand and utility of a cryptocurrency (utility of bitcoin is the possibility of moving digital money).

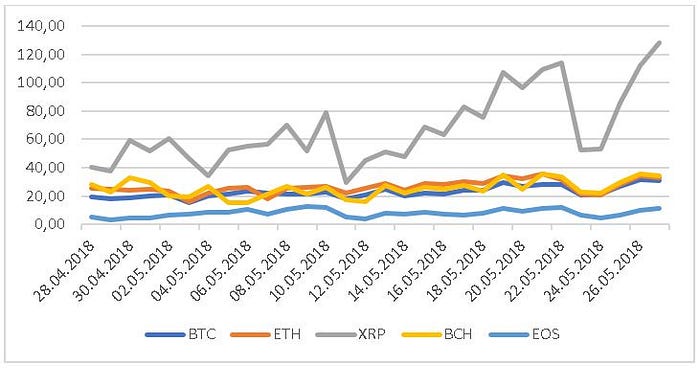

From an investors view we want to see the currency experiencing an above average amount of transcation volume. Therefore we use the so called ‚network value-to-transaction ratio‘ (NVT) to measure under/overvaluation of crypto assets. The network value equals the price of an assets times its circulating supply and is divided by the transcation volume in USD of the last 24h. According to the following figure NVT value for Ripple (XRP) has the highest value and volatilty with Bitcoin revealing the most stable development.

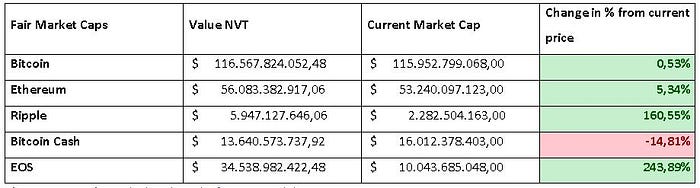

Taking into account the market capitalization of the largest five cryptocurrencies ($226.777.890.776,00) and an average 24h transactionvolume of $9.132.314.000,00 we calculate a peer-group NVT value of 24,83. In the following step we multiply the KPI with the 24h transaction volume of each cryptocurrency to determine their fair market cap according to this model.

Basically except for Bitcoin Cash every other cryptocurrency reveals an upward potential with EOS being the most undervalued cryptocurrency (potential = +243,89 %)

Nevertheless these calculations do not serve as an investment recommendation as the cryptocurrency market is subject to high volatility and price shocks regarding certain unpredictable events (regulation, hacker events, etc.).

3.3 Monte Carlo Simulation

Bitcoin prices follow highly volatile paths which makes future price predictions extremley difficult. A commonly used statistical tool for better decision making under uncertainty is running Monte Carlo simulations on historical data to estimate risk. Our approach is based on the geometric brownian motion (GBM), a model that is widely used for stock price forecast.

The GBM follows a random process whose future probalility distribution is determined by the most recent historical values.

In our model we use the latest BTC price ($7.711,17: 07.07.2018) and assume that the price will drift up by the expected return. We implement a random shock (‚up-or-down movement‘) that is defined as the standard deviation multiplied by a random number ‚x‘ we use to scale standard deviation.

These results will look differently every time we conduct a monte carlo simulation on our dataset. Our simulation predicts a mean Bitcoin (Ether) price of $43.477,70 ($6.655,02) in one year and a range from $1.232,24 to $861.250,98 ($141,98 to $76.686,16). Interisting is the analysis of the quantile functions. With 95 % of certainty we can say that the Bitcoin price will be between $4.881,38 ($909,32) and $138.501,51 ($20.732,58) in one year. Another interestig metric is the probability of a price equal or lower than the current market price. We calculated the distribution function and derived the cummulated probability of such an event with the result that the Bitcoin price will fall below the June, 7 value with a chance of 11,50 % (23,80 %).

These results do not provide any kind of investment recommendation but a scientific analysis of the underlying risk in investing into cryptocurrencies.

4. Summary

Our results reveal a rather upwards potential in the price of Bitcoin within a range of $39,54 — $37.714,66. Surely the models do not represent an exact valuation of Bitcoin but provide a mathematically founded approach to evaluate current valuation in cryprocurrency market. The models combine a valuation perspective with a risk perspective leading to a range of possible future outcomes with no exact prediction.

Future price development will be influenced by several external factors like political changes, changes in legal frameworks, cyber security and especially technological change. It is important to distinguish between the currency itself and the underlying technology, blockchain, which has a significant potential and use cases in several industries.

Carlos Arad is a FinTech Analyst for micobo GmbH. You can contact him via e-mail (ca@micobo.com)

References:

1. https://www.stromauskunft.de/strompreise/was-kostet-strom/; access: 11.06.2018

2. https://www.coinwarz.com/difficulty-charts/bitcoin-difficulty-chart: 11.06.2018